The CBIC has made major amendments to the GST refund mechanism through Notification No. 13/2025 – Central Tax dated 17th September 2025 (CGST Third Amendment Rules, 2025).

These changes, effective 1st October 2025, focus on faster refunds, risk-based scrutiny, and simplified revalidation requirements.

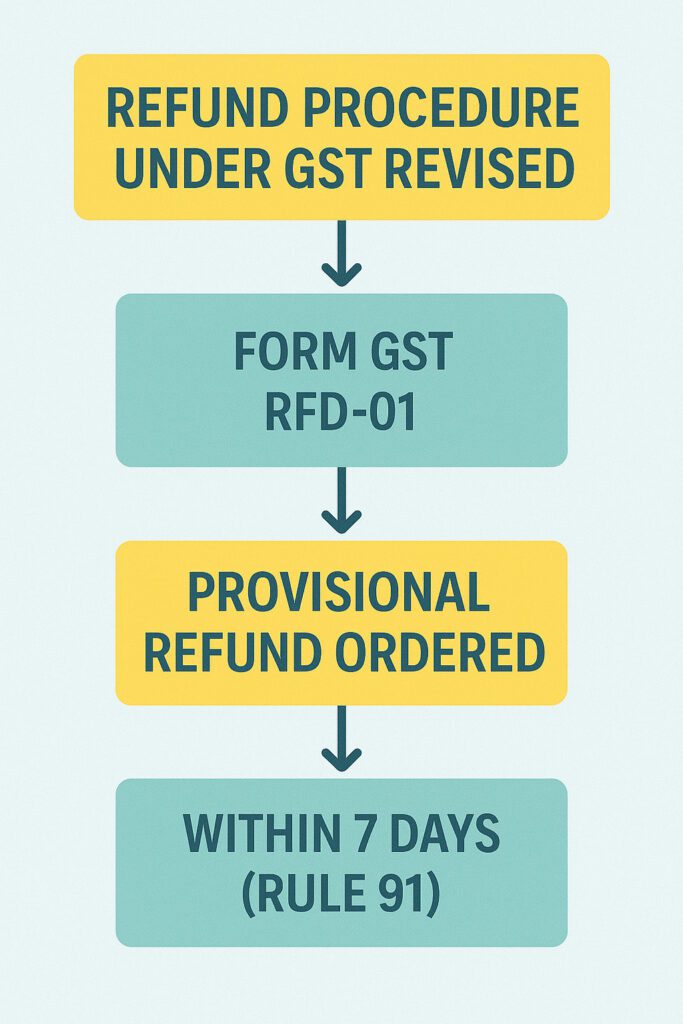

In this Handout, we decode the new refund procedure under Rule 91 and its impact on taxpayers.

1. Background of Rule 91

Rule 91 of the CGST Rules deals with grant of provisional refund.

Earlier:

- Proper officer was required to issue a provisional refund order in Form GST RFD-04 within 7 days from acknowledgement of refund application.

- If refund was delayed, revalidation of RFD-04 was required, causing unnecessary compliance burden.

2. Key Changes under Notification No. 13/2025

(a) Refund order timeline retained – 7 days

The proper officer must continue to issue Form GST RFD-04 within 7 days of acknowledgement (Rule 90).

(b) Risk-based scrutiny introduced

- Refund will now be subject to system-driven risk identification and evaluation.

- If flagged, officer may record reasons in writing and deny provisional refund, moving the case to detailed scrutiny under Rule 92.

📌 Impact: Ensures only genuine cases get faster refunds; riskier claims face extra checks.

(c) No revalidation required for RFD-04

Earlier, if RFD-04 was not processed within validity, revalidation was mandatory.

Now: Once issued, RFD-04 stands valid until final order, removing procedural hassles.

3. Updated Legal Text (Simplified)

Amended Rule 91(2) now reads:

“The proper officer, on the basis of identification and evaluation of risk by the system, shall make an order in FORM GST RFD-04, within a period not exceeding seven days from the date of acknowledgement… Provided that the proper officer, for reasons to be recorded in writing, may not grant refund on provisional basis and proceed under Rule 92. Provided further that the order issued in FORM GST RFD-04 shall not be required to be revalidated.”

4. Practical Impact on Taxpayers

(i) Faster Refunds for Compliant Taxpayers

- Low-risk applicants (regular filers, consistent compliance history) will continue to get refunds within 7 days.

(ii) Higher Scrutiny for Risky Refund Claims

Refund applications flagged by system may include:

- Excess ITC accumulation from suspicious suppliers.

- Large refund claims disproportionate to turnover.

- Frequent amendments in GSTR-3B.

These cases may be denied provisional refunds and moved to regular verification under Rule 92.

(iii) Reduced Compliance Burden

- No revalidation requirement saves time for both taxpayers and officers.

- Ensures refund process is smooth once provisional refund order is issued.

5. Example for Better Understanding

Before Amendment (Old Rule 91):

- Taxpayer files refund claim on 1st October 2025.

- Provisional refund order in RFD-04 issued on 5th October 2025.

- If refund was delayed and order expired, taxpayer had to chase officer for revalidation.

After Amendment (New Rule 91):

- Same taxpayer files claim on 1st October 2025.

- Refund processed by system as low-risk.

- RFD-04 issued on 5th October 2025 — valid until final refund order.

- No revalidation required even if final refund takes longer.

6. Compliance Tips for Taxpayers

- Ensure clean ITC records – Avoid excess/unjustified ITC claims to stay out of “risky” category.

- Reconcile GSTR-2B with GSTR-3B before filing refund.

- Maintain supplier compliance checks – if supplier defaults, your refund may get flagged.

- Track refund applications on GST portal – provisional order should come within 7 days.

Keep documentation ready – export invoices, LUTs, and ITC ledgers to defend refund claim if moved to Rule 92.

Key Takeaways

- Refunds to be issued within 7 days — but now system risk analysis applies.

- Low-risk taxpayers benefit, while risky claims face more scrutiny.

- Revalidation of RFD-04 no longer required, simplifying refund process.

- Businesses must maintain robust ITC documentation and compliance discipline.