Every GST-registered taxpayer must comply with the law — but sometimes mistakes happen. When tax is unpaid, short paid, or ITC is wrongly claimed, the department can issue notices and orders under Section 73 (non-fraud cases) or Section 74 (fraudulent cases).

This handout covers:

✅ Time limits for issuing SCN and orders

✅ Difference between Section 73 and 74

✅ GST penalty structures

✅ Practical examples

✅ Legal exceptions to time limits

✅ Image prompts for visual learning

Section 73 vs. Section 74 – What’s the Difference?

| Basis | Section 73 | Section 74 |

| Nature of Case | Non-fraud cases | Fraud / Willful misstatement / Suppression |

| Intent to evade tax | Not present | Present |

| Penalty Amount | Lower | Higher |

| Time limit to issue SCN & Order | Shorter | Slightly extended |

Time Limits for Issuance of SCN and Order

The time limit for issuing a Show Cause Notice (SCN) and Order under both sections is defined under the CGST Act. The relevant provision says:

- Section 73 – for cases where no fraud is involved.

- Section 74 – for fraud or suppression of facts with intent to evade tax.

The time limit is calculated from the due date of filing annual return (GSTR-9) of the relevant financial year.

Summary Table: Time Limits under Section 73 & 74

| Financial Year | GSTR-9 Due Date | Section 73 – SCN | Section 73 – Order | Section 74 – SCN | Section 74 – Order |

| 2017–18 | 5-Feb-20 | 30-Sep-23 | 31-Dec-23 | 5-Aug-24 | 5-Feb-25 |

| 2018–19 | 31-Dec-20 | 31-Jan-24 | 30-Apr-24 | 30-Jun-25 | 31-Dec-25 |

| 2019–20 | 31-Mar-21 | 31-May-24 | 31-Aug-24 | 30-Sep-25 | 31-Mar-26 |

| 2020–21 | 28-Feb-22 | 30-Nov-24 | 28-Feb-25 | 31-Aug-26 | 28-Feb-27 |

| 2021–22 | 31-Dec-22 | 30-Sep-25 | 31-Dec-25 | 30-Jun-27 | 31-Dec-27 |

| 2022–23 | 31-Dec-23 | 30-Sep-26 | 31-Dec-26 | 30-Jun-28 | 31-Dec-28 |

| 2023–24 | 31-Dec-24 | 30-Sep-27 | 31-Dec-27 | 30-Jun-29 | 31-Dec-29 |

Important Notes & Exceptions

- Section 76 – Tax Collected but Not Paid

👉 No time limit for issuance of notice or order. - Court/Tribunal Stay

👉 The period of stay is excluded from limitation. - Erroneous Refund

👉 3 years (Section 73) or 5 years (Section 74) counted from refund order date, not GSTR-9 due date.

Penalty Structure under Section 73 & 74

The penalty amount varies significantly based on:

- When the taxpayer pays the liability

- Whether the case involves fraud or not

Here’s how it works:

| Action by Taxpayer | Penalty under Section 73 | Penalty under Section 74 |

|---|---|---|

| Paid before SCN | No penalty | 15% of tax |

| Paid within 30 days of SCN | No penalty | 25% of tax |

| Paid within 30 days of Order | 10% of tax or ₹10,000 (whichever is higher) | 50% of tax |

| Paid after 30 days of Order | 10% of tax or ₹10,000 (whichever is higher) | 100% of tax |

Practical Examples

Example 1 – Section 73: Non-Fraud Case

Mr. A forgets to pay ₹50,000 GST due to incorrect computation. Department issues SCN under Section 73 on 25-Aug-2024.

- If he pays before SCN → No penalty

- If he pays within 30 days of SCN → No penalty

- If he pays after Order → 10% or ₹10,000 penalty

Example 2 – Section 74: Fraudulent Claim of ITC

A company wrongfully avails ₹1,00,000 ITC using fake invoices. Department issues SCN under Section 74.

- Pays before SCN → Penalty = ₹15,000

- Pays within 30 days of SCN → Penalty = ₹25,000

- Pays after Order → Penalty = ₹50,000 to ₹1,00,000

Legal Backing

These provisions are covered under:

- Section 73 & 74 of CGST Act, 2017

- Rule 142 of CGST Rules – Notice and order issuance procedure

- Section 76 – No time limit in cases of tax collected but not deposited

Various Circulars/Instructions issued by CBIC

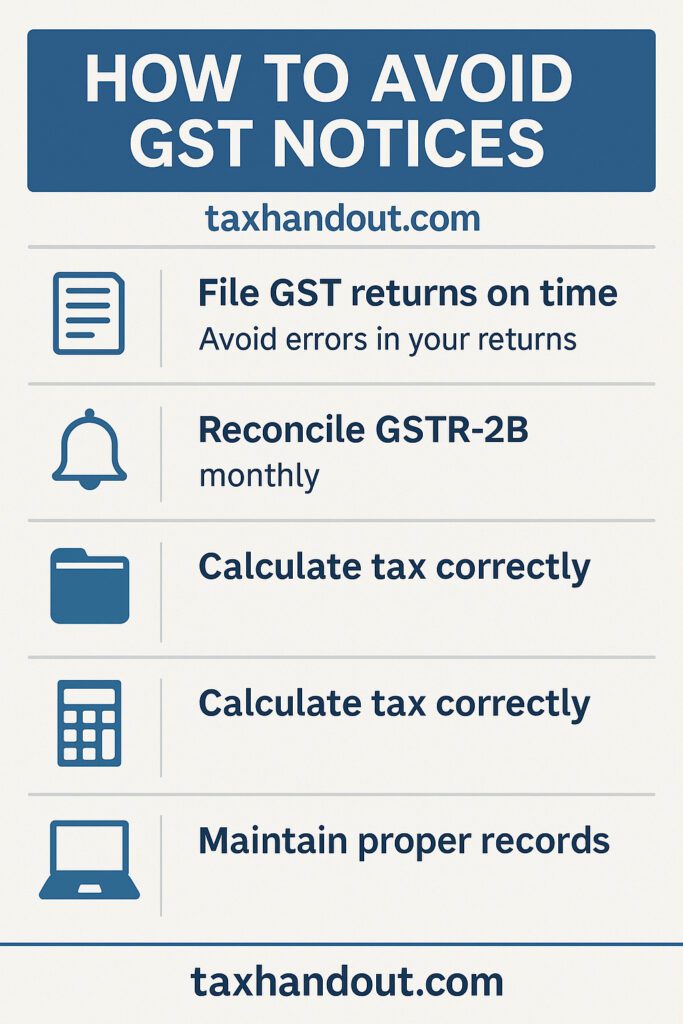

Tips to Avoid Notices under Section 73/74

- File accurate and timely GSTR-1 & GSTR-3B

- Reconcile GSTR-2B with books monthly

- Avoid claiming ineligible ITC

- Maintain proper documentation for ITC eligibility

Never ignore DRC-01 notices on the portal

FAQs

Q1: Can I still get a notice after 3 years for a non-fraud case?

Answer: No, unless it falls under exceptions like Court Stay or Refund.

Q2: Can I voluntarily pay tax to avoid penalty?

Answer: Yes. If you pay tax and interest before SCN, penalty under Section 73 becomes nil, and under Section 74 it is limited to 15%.

Q3: What if I received a DRC-01 but paid tax within 30 days?

Answer: You can avoid higher penalties. Under Section 73, no penalty. Under Section 74, penalty is 25%.

Q4: Is interest also waived if tax is paid early?

Answer: No. Interest under Section 50 is always applicable until payment is made.

Conclusion

Understanding time limits and penalty structures under Sections 73 & 74 is crucial for every GST-registered person. By proactively managing compliance and acting swiftly when notices are received, you can reduce financial exposure and legal complications.

Stay updated with GST timelines and respond timely to Show Cause Notices (SCNs).

![GST on Education Services: What’s Exempt & What’s Not? [2025 Updated List]](https://taxhandout.com/wp-content/uploads/2025/07/Gst-on-Education-Services.svg)