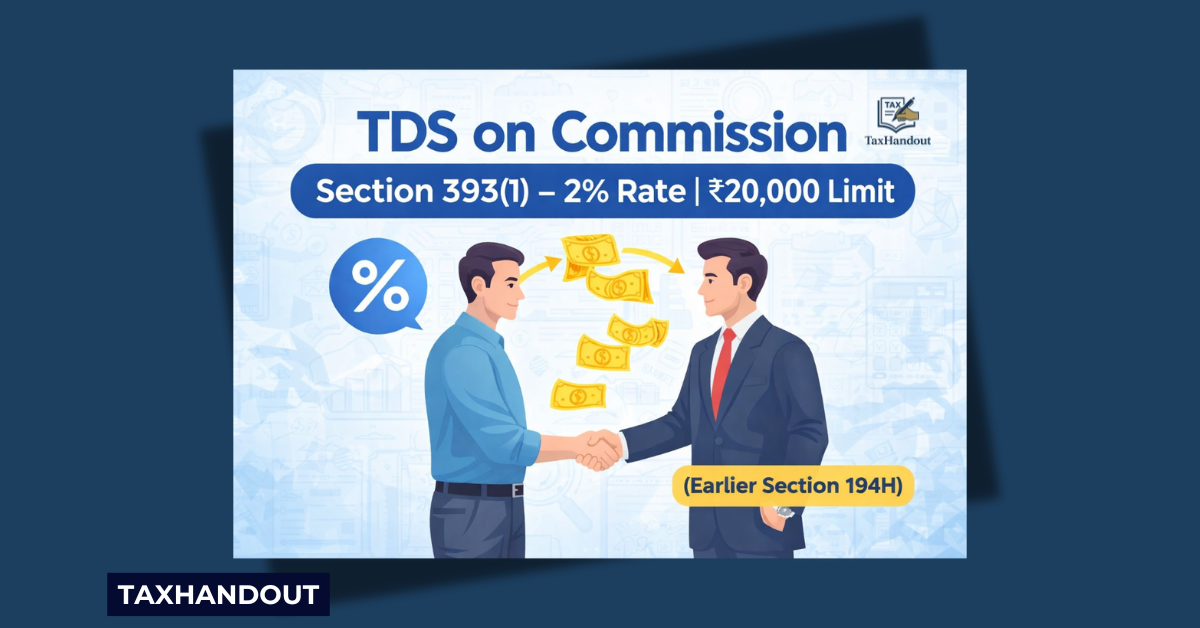

TDS on commission or brokerage is one of the most commonly applicable provisions in day-to-day business transactions. Under the Income Tax Act, 2025, this provision is now covered under Section 393(1) TSN 1(ii) (earlier Section 194H).

If you are making payments to agents, brokers, or intermediaries, this section becomes directly applicable and mistakes here are very common.

This handout explains the provision in a simple and practical manner.

Basic Overview of Section 393(1) TSN 1(ii)

| Particulars | Details |

| Section | 393(1) TSN 1(ii) |

| Nature of Payment | Commission or Brokerage |

| Payer | Any person |

| Payee | Resident |

| TDS Rate | 2% |

| Time of Deduction | At the time of credit or payment, whichever is earlier |

| Threshold Limit | ₹20,000 (annual) |

What is Commission or Brokerage?

As per Section 402(7) (definition clause under new Act):

Commission or brokerage includes any payment received or receivable, directly or indirectly, by a person acting on behalf of another person for:

- Services rendered (other than professional services), or

- Services in the course of buying or selling goods, or

- Transactions relating to any asset, valuable article, or thing (excluding securities)

Practical Meaning

In simple terms:

- If someone helps you get business, sales, or clients, and you pay them a percentage → This is commission

- If someone acts as a middleman between buyer and seller → This is brokerage

When is TDS Required to be Deducted?

TDS must be deducted when:

- Total commission or brokerage exceeds ₹20,000 in a financial year, and

- Payment is made to a resident person, and

- Payment is not in the nature of professional services

Time of Deduction

TDS should be deducted:

- At the time of credit in books, OR

- At the time of actual payment

Whichever is earlier

Rate of TDS – Important Note

- Standard Rate: 2%

- If PAN is not available → higher rate may apply as per general provisions

Transactions Covered (Practical Examples)

| Scenario | TDS Applicable? |

| Sales commission to agent | Yes |

| Brokerage to property dealer | Yes |

| Referral commission | Yes |

| Discount given to customer | No |

| Salary incentives to employees | No |

Important Exception (Section 393(4))

No TDS is required in the following case:

- Commission or brokerage paid by:

- Bharat Sanchar Nigam Limited (BSNL), or

- Mahanagar Telephone Nigam Limited (MTNL)

- To their public call office (PCO) franchisees

Section 393(1) TSN 1(ii) may look simple, but in practice, it creates multiple compliance issues—especially in identifying whether a payment is commission or not.

A wrong classification can directly lead to tax disallowance and litigation.

Businesses should properly review all commission-related transactions and ensure timely TDS deduction.