Imagine this.

You log into your GST portal after a few weeks…

And suddenly you see multiple assessment orders already passed.

No reply filed.

No hearing attended.

And worst part—you didn’t even know notices were issued.

Sounds extreme? It’s not. This happens more often than professionals admit.

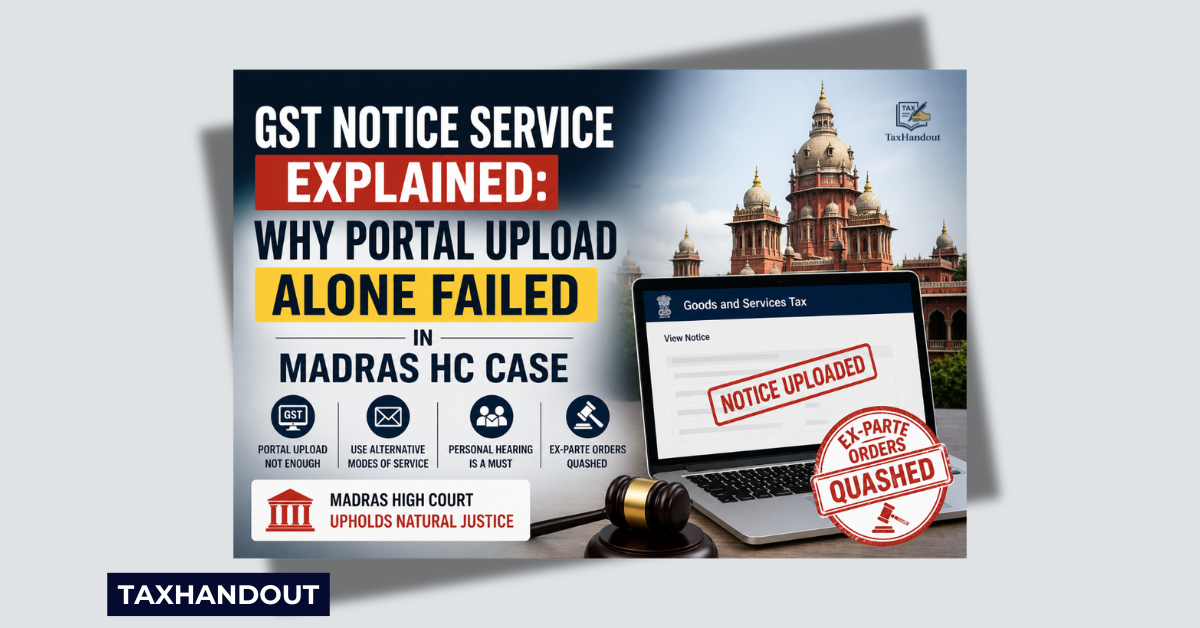

In a significant ruling, the Madras High Court in Praveen Constructions vs State Tax Officer (06-02-2026) has addressed this exact issue—and sent a strong message to the department.

What Actually Happened

- Department uploaded show cause notices only on GST portal

- Taxpayer never became aware

- No reply was filed (obviously)

- Officer passed 6 assessment orders in January 2025

- No personal hearing was given

Now here’s the key question:

Can the department say—“We uploaded it, our job is done”?

The Court said—No.

Core Legal Questions

This case revolved around two critical issues:

1. Is GST Portal Upload Always a Valid Service?

Yes—technically.

But is it always effective?

The Court said—not necessarily.

2. Can Ex-Parte Orders Be Passed Without Hearing?

Clear answer:

No hearing = violation of natural justice

And that makes the order weak.

What the Law Says

Section 169(1) – CGST Act (Service of Notice)

It allows multiple modes:

- Portal upload

- Registered Post (RPAD)

- Physical delivery

Here’s the mistake officers make:

They treat portal upload as the only method, not one of many options.

Section 75 – CGST Act

- Mandatory opportunity of being heard

- Ensures fair procedure

This is not optional compliance—it’s foundational.

Arguments by the Taxpayer

The assessee took a very realistic stand:

- Notices were only on portal

- No actual knowledge

- No hearing provided

- Orders passed mechanically

And importantly:

The taxpayer agreed to deposit 25% of disputed tax—showing bona fide intent.

Department’s Stand

Typical departmental defense:

- Notices uploaded on portal

- Taxpayer failed to check

- Hence, service is valid

But here’s where things collapsed:

- They admitted no personal hearing was given

- They agreed for remand subject to deposit

That weakened their own argument.

Madras High Court’s Observations

The Court didn’t just interpret law—it applied common sense.

1. Technical Compliance ≠ Effective Service

Yes, portal upload is legally valid.

But the Court clearly said:

If taxpayer is not responding, officer must ensure actual communication, not just system compliance.

2. Officers Must Use Alternative Modes (Section 169)

If no response:

- Use RPAD

- Try other modes

- Ensure notice actually reaches taxpayer

Otherwise, it becomes a “formality exercise”—not real service.

3. Personal Hearing is a Legal Right

No hearing given = serious flaw.

This alone can invalidate the entire proceeding.

4. Mechanical Orders Waste Everyone’s Time

The Court openly criticized this approach:

- Leads to avoidable litigation

- Burdens courts

- Delays justice

The High Court passed a balanced order:

Relief to Taxpayer

- All 6 assessment orders set aside

- Case remanded for fresh consideration

Conditions Imposed

- Taxpayer must deposit 25% of disputed tax within 4 weeks

Directions to Department

- Give 14 days clear notice

- Provide proper personal hearing

Pass fresh order on merits