When a taxpayer sells property, shares, or any capital asset, capital gain tax becomes applicable.

However, the Income Tax Act provides multiple exemptions which can legally reduce or eliminate tax, if planned correctly.

With the introduction of the Income Tax Act, 2025:

- Section numbers have been reorganized into 120 series

- Core provisions remain largely unchanged

- Focus now is on limits, timelines & structured compliance

SECTION MAPPING – 1961 vs 2025 ACT

| Old Section | New Section (2025) | Purpose |

| 54 | 124 | House to House |

| 54B | 123 | Agricultural Land |

| 54D | 122 | Compulsory Acquisition |

| 54EC | 126 | Bonds |

| 54F | 125 | Other Asset to House |

| 54G | 127 | Business Shift (Rural) |

| 54GA | 128 | Shift to SEZ |

| 54EE | 129 | Specified Funds |

| 54GB | 130 | Startup Investment |

SECTION-WISE COMPLETE ANALYSIS

1. Section 54 → Section 124 (Residential House)

Applies when residential house is sold

- Eligible: Individual / HUF

- Investment: 1 residential house in India

Time Limit:

- Purchase → 1 year before / 2 years after

- Construction → 3 years

Exemption:

- Full or proportionate

Key Highlights:

- ₹10 Crore maximum exemption cap

- Option to buy 2 houses (once) if gain ≤ ₹2 Cr

- CGAS applicable if not invested before due date

2. Section 54B → Section 123 (Agricultural Land)

Sale of agricultural land used for last 2 years

- Eligible: Individual / HUF

- Investment: New agricultural land

3. Section 54D → Section 122 (Compulsory Acquisition)

Time limit: 2 years

Industrial land/building acquired by Government

- Investment in new industrial asset allowed

- Rare but important

4. Section 54EC → Section 126 (Bonds Investment)

Sale of land/building → invest in bonds

- Eligible: All taxpayers

Investment in:

- National Highways Authority of India

- Rural Electrification Corporation

Time limit: 6 months

Key Features:

- ₹50 lakh cap

- 5-year lock-in

- Loan/transfer → exemption reversed

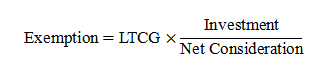

5. Section 54F → Section 125 (Other Assets)

Sale of shares, plot, gold, etc.

- Eligible: Individual / HUF

- Investment: Residential house

Exemption Formula:

Important Conditions:

- Full exemption only if entire sale proceeds invested

- Must not own more than 1 house

- New house sale within 3 years → exemption reversed

- ₹10 Crore cap applies

6. Section 54G → Section 127 (Urban → Rural Shift)

Business shifting from urban to rural area

- Investment in plant, machinery, land

7. Section 54GA → Section 128 (Shift to SEZ)

Similar to 54G

Applicable when shifting to SEZ

8. Section 54EE → Section 129 (Specified Funds)

Investment in Government-notified funds

- ₹50 lakh cap

- 3-year lock-in

- Rare in practice

9. Section 54GB → Section 130 (Startup Investment)

Capital gain invested in eligible company/startup

- Useful for business restructuring

REINVESTMENT LIMITS & LOCK-IN SUMMARY

| Category | Old Sec. | New Sec. | Limit | Lock-in |

| Residential House | 54 | 124 | ₹10 Cr | 3 Years |

| Non-House Asset | 54F | 125 | ₹10 Cr | 3 Years |

| Bonds | 54EC | 126 | ₹50 Lakh | 5 Years |

| Funds | 54EE | 129 | ₹50 Lakh | 3 Years |

DEEP DIVE – CRITICAL PROVISIONS

1. ₹10 Crore Ceiling (Sec 124 & 125)

Maximum exemption = ₹10 Crore

Practical Example:

- Gain = ₹50 Cr

- Investment = ₹40 Cr

Exemption = ₹10 Cr

Balance investment → no benefit

2. Two-House Benefit (Once in Lifetime)

Applicable if gain ≤ ₹2 Cr

Can buy 2 houses

Only once in lifetime

3. Net Consideration Trap (Sec 125)

Most misunderstood provision

- Section 124 → invest gain

- Section 125 → invest full sale value

Partial investment = proportionate exemption

COMPLIANCE CHECKLIST

1. CGAS Requirement

If not invested before ITR due date:

Must deposit in Capital Gains Account Scheme

Otherwise → entire gain taxable

2. Lock-in Compliance

| Asset | Lock-in |

| House | 3 Years |

| Bonds | 5 Years |

| Funds | 3 Years |

Early sale = exemption reversed

3. LTCG Holding Period

| Asset | Period |

| Property | 24 Months |

| Unlisted Shares | 24 Months |

| Listed Shares / MF | 12 Months |

Very Helpful