Most taxpayers who lose GST cases on technical grounds don’t lose because the law was against them — they lose because nobody on their side understood Section 169. A show cause notice sits unread in the “Additional Notices and Orders” tab of the GST portal. An order is uploaded at 5 p.m. and confirmed the next morning. An accountant who left the firm eight months ago was the only one with the registered email’s password. By the time the taxpayer finds out, the limitation period to appeal has often already run out.

Section 169 of the CGST Act, 2017 is the provision that decides whether any of that matters. It governs how notices, summons, and orders must be served, and — just as importantly — when service is deemed to have happened even if nobody actually read the document. Because so much of GST litigation eventually turns on one question — “was this notice validly served?” — every GST practitioner, in-house finance team, and tax officer needs a working command of this section, not just a textbook acquaintance with it.

This guide walks through the bare provision clause by clause, explains what “deemed service” really means, examines whether a portal upload alone is ever enough, and analyses Haryana’s freshly issued Instruction No. 02/2026/GST-II dated 01.06.2026, which has reopened the debate on physical intimation of notices. It closes with the High Court trend on ex-parte orders, practical checklists, and answers to the questions practitioners ask most often.

Why Section 169 Matters More Than It Looks

On paper, Section 169 is a procedural, almost administrative provision — a list of acceptable delivery methods. In practice, it is one of the most litigated sections in the entire GST framework, because it sits at the intersection of two competing interests. The department needs a workable, low-cost way to communicate with crores of registered taxpayers, most of whom interact with the GST system only through the common portal. The taxpayer needs a genuine, fair opportunity to know that proceedings have been initiated against them before their liability crystallises or their right to appeal lapses.

Section 169 tries to resolve that tension by offering the department several alternative modes of service and then attaching a legal fiction — deemed service — to each of them. The difficulty is that “deemed served” and “actually known” are not the same thing, and Indian courts have spent the better part of the last five years working out how far that gap can be allowed to stretch before it tips into a violation of natural justice. That is the entire battlefield this article maps.

Legislative Background and Its Relationship with Natural Justice

Section 169 was drafted with a clear administrative objective: to give GST officers a standardised, defensible way to serve documents in an era where most compliance has moved online, without forcing every notice through the slow and expensive route of physical registered post. Read in isolation, it is a fairly mechanical clause modelled on similar service provisions in the erstwhile VAT and Central Excise laws, adapted for an electronic-first regime. The complication is that GST adjudication carries real consequences — demand confirmation, recovery, registration cancellation, blocking of input tax credit — and Article 14 and Article 21 jurisprudence has long held that no civil consequence can be visited on a person without a genuine opportunity to be heard. Section 169 therefore cannot be read as a standalone, self-contained code. It operates alongside Section 75(4) (which mandates an opportunity of hearing in adverse orders) and the constitutional principle of audi alteram partem. Courts have repeatedly had to decide where the line falls between “the department followed Section 169 to the letter” and “the taxpayer was actually given a fair chance to respond” — and, as this guide shows, those two things are not always the same.

Section 169 Explained Clause by Clause

Section 169(1) lists six modes through which any decision, order, summons, notice, or other communication under the Act may be served. The clauses are framed as alternatives — the department is not required to attempt them in sequence, with one important exception built into clause (f).

Clause (a) — direct tendering. The notice may be handed over directly or through a messenger (including a courier) to the taxable person, or to their manager, authorised representative, advocate, or tax practitioner, or to any adult family member residing with them, or to a person regularly employed by them. Example: a GST inspector hands a physical copy of a summons to the office accountant during a visit — that is valid service even though the proprietor never personally received it.

Clause (b) — registered post, speed post, or courier with acknowledgement due. Sent to the last known place of business or residence. Example: an order sent by speed post to an address the taxpayer vacated two years ago, without updating GST registration records, is still treated as sent to the “last known” address — which is precisely why keeping registration details current matters so much.

Clause (c) — email. Sent to the email address provided at registration, or as amended. Example: a notice emailed to an ID that has since been deactivated by the company’s IT department, with no bounce-back monitored by anyone, technically satisfies clause (c) even though it never reached a human being.

Clause (d) — the common portal. Made available on the GST common portal after generation of a unique reference number. This is, in practice, the default and most heavily used mode today, since every adjudication notice and order is in any event uploaded to the portal as part of the workflow.

Clause (e) — newspaper publication. Publication in a newspaper circulating in the locality of the taxpayer’s last known place of business or residence.

Clause (f) — affixation, as a last resort. Only “if none of the modes aforesaid is practicable” — affixing a copy at the last known place of business or residence, and if even that is not practicable, affixing it on the notice board of the office of the officer who passed the order. This is the one clause that is explicitly conditional on the other modes having failed; it is not a free-standing alternative the way (a) through (e) are treated.

What Is “Deemed Service” Under Section 169(2) and (3)?

Sub-section (2) creates a legal fiction: a notice is deemed served on the date it is tendered, published, or affixed in the manner described above — irrespective of whether the taxpayer has actually opened, read, or even noticed it. For service by post, the deeming provision works alongside Section 27 of the General Clauses Act, under which service is presumed complete at the time the letter would ordinarily be delivered in the course of post, unless the contrary is proved.

Sub-section (3) deals specifically with electronic communication and largely mirrors Sections 13(2) and 13(3) of the Information Technology Act, 2000: where the addressee has designated a computer resource for receiving electronic records, service is deemed complete the moment the record enters that resource — not when the addressee actually opens or reads it. Where no resource has been designated, service is deemed complete only when the addressee retrieves the record. This distinction — “entered the system” versus “actually retrieved” — has become one of the most contested legal questions in GST litigation in 2025–26, because the GST portal arguably functions as a designated resource for clause (d) service, but whether the same logic extends to a simple email under clause (c) is far less settled.

In practical terms: the law does not require the taxpayer to have actually read the notice for service to be “complete.” It requires only that the department followed one of the prescribed modes correctly. That is precisely why so many disputes end up in the High Courts — taxpayers arguing they were deprived of a fair hearing despite technically valid service, and departments arguing that deemed service is conclusive once a mode under Section 169(1) has been correctly followed.

Is Uploading on the GST Portal Alone Sufficient?

This is the single most litigated question under Section 169, and the honest answer is: it depends on which High Court you ask, and the law is still moving.

The department’s consistent position is that clause (d) is a free-standing, independent mode of service. Since every registered taxpayer is obligated to log in and monitor the portal as part of ordinary GST compliance, uploading a notice there — generating a unique reference number in the process — is by itself sufficient and final. Several Madras High Court benches have accepted a version of this reasoning, holding in cases such as Pandidorai Sethupathi Raja v. Superintendent of Central Tax that it is the taxpayer’s own obligation to monitor the portal, and that posting on it is sufficient compliance without any further alert being necessary. The Calcutta High Court reached a broadly similar conclusion in Carry Co. v. Union of India (June 2025), holding that uploading an order on the portal validly constitutes service under clause (d), and that the six clauses of Section 169(1) need not be exhausted sequentially — only clause (f) carries that sequential, last-resort condition.

Set against this is a competing line of reasoning, also from the Madras High Court, that reads the six clauses far more conjunctively. In a widely discussed 2025 ruling, the Court held that the statute “mandates” service in person, by registered post, or by email as the primary modes, and that publication on the portal (or in a newspaper) is meant to be a fallback used only when those primary modes fail or prove impracticable — echoing the structure that clause (f) makes explicit for affixation. On this reading, Rule 149’s framework for purely electronic service cannot override the wider menu the parent statute itself provides.

Valid Service vs. Opportunity of Being Heard vs. Natural Justice

This is where most practitioners blur three concepts that are legally distinct, and the confusion costs taxpayers real cases.

Valid service of notice is a narrow, mechanical question: did the department use one of the modes listed in Section 169(1), correctly? If yes, service is deemed complete under sub-section (2), regardless of what happened afterward.

Opportunity of being heard is a separate, substantive requirement under Section 75(4) — the taxpayer must be given a genuine chance to respond before an adverse order is passed, including a personal hearing where requested or where an adverse decision is contemplated. A notice can be validly “served” under Section 169 and still fail to provide a real opportunity of hearing — for instance, where the gap between service and the hearing date is unreasonably short, or where a reply is filed but never actually considered before the order is passed.

This is exactly the gap the Jharkhand High Court exposed in NKAS Services (P) Ltd. v. State of Jharkhand (2021–22). The Court did not find fault with how the notice was served; it found that the show cause notice itself — issued through the standard DRC-01 summary format — was so vague and devoid of specific allegations that it could not function as a proper notice under Section 73/74 at all, regardless of valid service, because the taxpayer was never told what case it actually had to meet. Several subsequent Jharkhand rulings, including Godavari Commodities Ltd. (2022) and Alok Steel Industries (2023), have applied the same reasoning.

Principles of natural justice sit above both of these as the constitutional umbrella — audi alteram partem and the rule against bias. A proceeding can technically satisfy both Section 169 (valid service) and Section 75(4) (an opportunity was offered) and still be struck down if, on the facts, the process was not genuinely fair — for example, where an officer mechanically rejects a reply without recording any reasons, or decides a matter before the reply deadline has even passed.

The practical takeaway: arguing “service under Section 169 was defective” is the narrowest and often the hardest ground to win on, because courts increasingly defer to the department once any one of the six clauses is shown to have been followed. Arguing “I was denied a genuine opportunity of hearing despite service” or “natural justice was violated on these specific facts” tends to be the stronger, more fact-driven ground — and the one that actually moves High Courts to interfere.

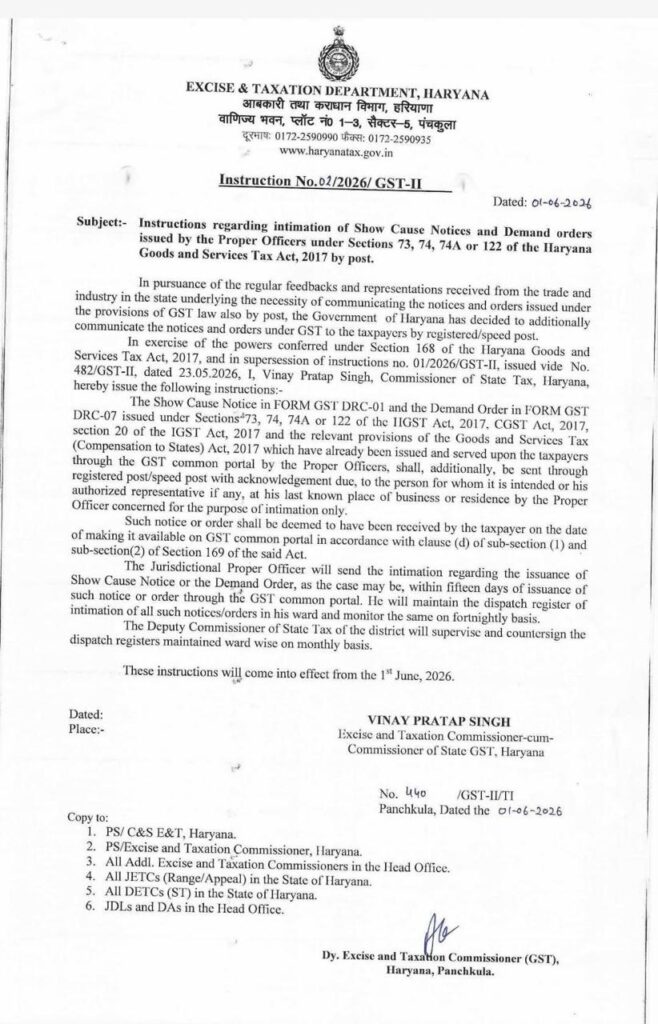

Haryana Instruction No. 02/2026/GST-II Dated 01.06.2026: What It Actually Changes

On 1 June 2026, the Excise and Taxation Department, Haryana, issued Instruction No. 02/2026/GST-II under Section 168 of the HGST Act, 2017, superseding the short-lived Instruction No. 01/2026/GST-II of 23 May 2026. The instruction responds to recurring complaints from trade and industry that notices uploaded only to the portal were being missed — because of technical glitches, the absence of any proactive alert, or a change in the staff member responsible for GST compliance.

Here is what it actually requires, and what it does not.

What it requires. Where a Show Cause Notice in Form GST DRC-01, or a Demand Order in Form GST DRC-07, has been issued under Sections 73, 74, 74A, or 122 of the HGST Act (and the corresponding provisions of the CGST Act, IGST Act, and the GST Compensation to States Act) and has already been made available on the common portal, the Proper Officer must additionally send a postal intimation — by Registered Post or Speed Post with Acknowledgement Due — to the taxpayer, or their authorised representative, at the last known place of business or residence. This dispatch must happen within 15 days of the notice or order being issued on the portal. Officers are required to maintain ward-wise dispatch registers recording every such postal intimation, and dispatches are to be tracked fortnightly. The Deputy Commissioner of State Tax for the district is responsible for overseeing compliance and countersigning the dispatch registers.

What it deliberately does not change. The instruction is explicit that the postal intimation is supplementary and exists “solely for the purpose of intimation.” The legal date of service — and therefore the start of any limitation period for filing a reply or an appeal — continues to be governed entirely by Section 169 of the CGST/HGST Act, and remains the date the notice or order is made available on the common portal. Postal dispatch, even if delayed or skipped entirely, does not extend the limitation period available to the taxpayer, and does not retroactively shift the date of “service” for legal purposes.

Why this matters, and why it is not an amendment to Section 169. An instruction issued under Section 168 is an internal administrative direction to officers — it binds the department’s own machinery on how to conduct itself, but it cannot amend, override, or add a new mode of service to a Central Act. Only Parliament can do that. So this instruction does not create a seventh mode of service, and a taxpayer cannot argue that Haryana orders are now invalid unless physically posted — Section 169(1)(d) remains good law in Haryana exactly as it is everywhere else.

Can taxpayers use a violation of this instruction in litigation? This is genuinely a grey area, and any confident answer should be treated with caution. Because the instruction does not alter the statutory mode of service, a court is unlikely to hold that proceedings are void purely because postal intimation was skipped or late, where portal service under clause (d) was otherwise valid. That said, administrative circulars of this kind have, in other GST contexts, been treated by courts as relevant — not decisive — evidence of what fair departmental practice looks like, and as a factor courts may weigh when an ex-parte order is challenged on natural-justice grounds, particularly where the taxpayer can show genuine non-receipt of the portal notice. Practically, this instruction is best read as Haryana building itself a stronger evidentiary record and a fairness cushion against future writ petitions — not as a new right that taxpayers can independently enforce.

High Court Trend: Why Ex-Parte GST Orders Keep Getting Set Aside

Even where Section 169 is technically complied with, High Courts have repeatedly quashed or remanded DRC-07 demand orders, ASMT assessment orders, and registration cancellation orders passed ex-parte. The recurring patterns are worth knowing because they predict where courts are willing to intervene:

Notices uploaded only under the “View Additional Notices and Orders” tab on the portal — a less visible section than the main dashboard — followed by an ex-parte order with no attempt at any other mode, have been set aside by the Madras High Court, which held that uploading alone is not enough if the officer makes no further effort once there is no response, and that communications after a voluntary registration cancellation must specifically go to the email on record. Show cause notices that are vague, templated, or fail to specify the actual contravention — even when validly served — have been struck down by the Jharkhand High Court in the NKAS Services line of cases discussed above, on the footing that a defective notice cannot found a valid order regardless of how it was delivered. Registration cancellations passed mechanically, without recording reasons or genuinely considering the taxpayer’s position, were quashed by the Gujarat High Court in Aggarwal Dyeing and Printing Works v. State of Gujarat (2022), a case still widely cited in 2026 for the proposition that vague notices and non-speaking orders breach natural justice independent of the service question.

The throughline across all of these: courts treat Section 169 compliance as a floor, not a ceiling. An officer who stops at “I uploaded it to the portal” and proceeds straight to an ex-parte order — without checking for a response, without attempting a second mode where the stakes are high, and without giving genuine reasons — is taking on real litigation risk, even in jurisdictions that otherwise accept portal-only service as valid in principle.

Practical Examples

Example 1 — the silent inbox. A notice is uploaded to the portal; the firm’s accountant, who used to check it weekly, left the company four months earlier and nobody reassigned the login. The order is passed ex-parte. Service is technically valid under clause (d); the taxpayer’s remedy lies in showing the order itself was passed without genuine application of mind, not in attacking the mode of service.

Example 2 — no time to respond. A notice is uploaded at 5 p.m. on a Friday, with the order passed the following Monday morning. Even where the underlying service is valid, this fact pattern is a strong natural-justice argument — the taxpayer was never realistically able to respond within the window actually available, regardless of what the notice’s stated deadline said.

Example 3 — the bounced email. A notice is sent under clause (c) to a company email that has since been deactivated, and the system shows a bounce-back the officer never checks. Whether this counts as valid service turns on the same unsettled “entered the system vs. actually retrieved” distinction discussed in the deemed-service section above.

Example 4 — cancellation without hearing. A GST registration is cancelled for non-filing of returns, with the show cause notice served only via the portal and the order passed without any personal hearing being offered, despite the taxpayer’s right to one under Section 75(4). This is the precise fact pattern the Gujarat High Court intervened on in Aggarwal Dyeing.

Example 5 — the stale email on file. A demand notice is sent to the email address provided at the time of original GST registration years earlier, even though the company’s GST profile was never updated after a change in the finance team. Clause (c) is, on its face, satisfied; the taxpayer’s argument has to be built around fairness and actual notice, not around the validity of the mode itself.

Section 169 looks like a housekeeping provision and behaves like a litigation minefield. The bare text gives the department six alternative ways to serve a document, attaches a deeming fiction to each, and asks for nothing more than that one of them be followed correctly. The complication taxpayers and practitioners alike keep running into is that valid service, a genuine opportunity of hearing, and the broader requirements of natural justice are three separate tests — and an order can pass one or two of them while failing the third.

Disclaimer: This article is for general informational purposes and reflects the law and reported judicial trend as of June 2026. It is not legal advice. Given that the Supreme Court’s final ruling on the Bambino Agro Industries question is pending, and several High Court positions remain in tension with each other, readers should obtain independent professional advice before relying on any position taken here in a specific matter.