GST registration is the backbone of every registered business. Once the registration is cancelled, the taxpayer loses the legal authority to collect GST, issue tax invoices, and claim Input Tax Credit (ITC). For many businesses, cancellation of registration can virtually bring operations to a standstill.

One of the most common reasons for cancellation is non-filing of GST returns.

Recognizing that many taxpayers eventually become compliant by filing pending returns and paying outstanding dues, the Government introduced an important relief through the proviso to Rule 22(4) of the CGST Rules, 2017. This provision enables cancellation proceedings to be dropped if the taxpayer clears all pending compliances before the cancellation order is passed.

Further, the Gauhati High Court in Smt. Bina Taipodia v. Union of India (2026) has reaffirmed that even after cancellation, authorities should consider restoration where the taxpayer has fulfilled all statutory obligations.

In this article, we will discuss:

- Legal provisions governing cancellation of GST registration

- Procedure for cancellation

- Proviso to Rule 22(4)

- Revocation of cancellation under Section 30

- Latest Gauhati High Court judgment

- Practical guidance for taxpayers

Legal Framework Governing Cancellation of GST Registration

The restoration of GST registration revolves around four important legal provisions:

- Section 29 of the CGST Act – Cancellation or suspension of registration.

- Rule 22 of the CGST Rules – Procedure for cancellation by the Proper Officer.

- Section 30 of the CGST Act – Revocation of cancellation.

- Rule 23 of the CGST Rules – Procedure for revocation.

Understanding the sequence of these provisions makes the entire process much easier.

When Can GST Registration Be Cancelled?

Section 29(2) empowers the Proper Officer to cancel GST registration under various circumstances.

Some common reasons include:

- Non-filing of GST returns.

- Registration obtained by fraud, wilful misstatement or suppression of facts.

- Business discontinued or transferred.

- Change in constitution of business.

- Contravention of GST provisions.

- Voluntary cancellation.

Among these, non-filing of returns is by far the most common reason.

Cancellation Due to Non-Filing of Returns

Section 29(2) specifically provides cancellation where:

Composition Taxpayer

Fails to furnish returns for the prescribed period under Section 29(2)(b).

Regular Taxpayer

Fails to furnish returns continuously for the prescribed period under Section 29(2)(c).

Once these conditions are satisfied, the Proper Officer may initiate cancellation proceedings.

Procedure for Cancellation Under Rule 22

Rule 22 lays down the complete procedure.

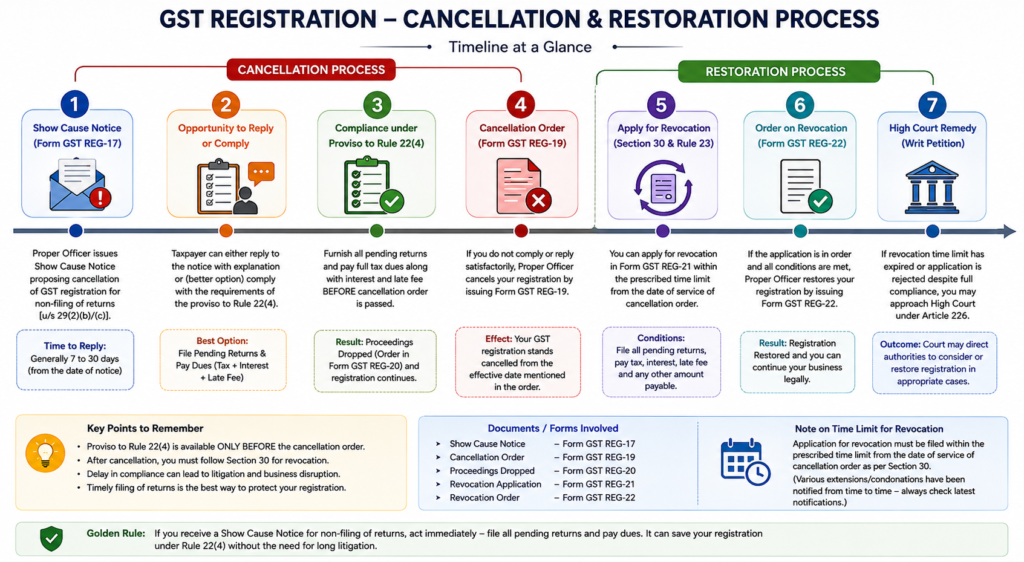

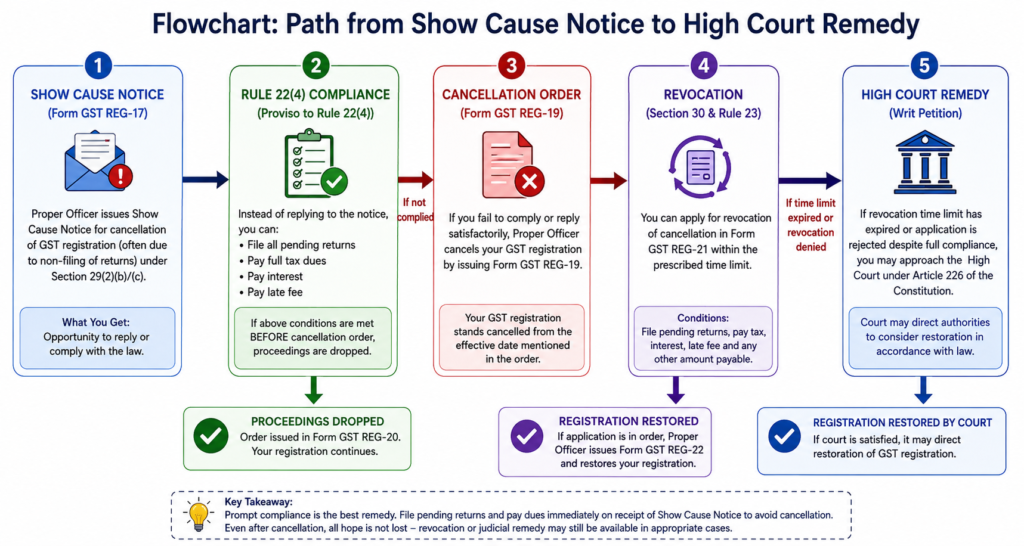

Step 1 – Issue of Show Cause Notice

The Proper Officer issues FORM GST REG-17, requiring the taxpayer to explain why registration should not be cancelled.

The notice specifies the reasons for proposed cancellation.

Step 2 – Reply by Taxpayer

The taxpayer may:

- submit a written reply,

- produce supporting documents,

- or rectify the default.

For cases involving non-filing of returns, the taxpayer now has a much simpler option because of the proviso to Rule 22(4).

Step 3 – Order by Proper Officer

After considering the reply and compliance, the Proper Officer may either:

- drop the proceedings, or

- cancel the registration through FORM GST REG-19.

Proviso to Rule 22(4): A Major Relief for Taxpayers

One of the most taxpayer-friendly amendments under GST is the insertion of the proviso to Rule 22(4).

The proviso states that where the cancellation notice has been issued for non-filing of returns under Section 29(2)(b) or Section 29(2)(c), the taxpayer may simply:

- furnish all pending returns,

- pay the entire tax liability,

- pay applicable interest,

- pay applicable late fee,

instead of filing a detailed reply.

Upon such compliance, the Proper Officer shall drop the cancellation proceedings by issuing FORM GST REG-20.

The use of the word “shall” makes this provision mandatory rather than discretionary, provided all the prescribed conditions are fulfilled.

Conditions to Avail the Benefit of Rule 22(4)

To obtain relief under this proviso, the following conditions must be satisfied:

- Cancellation must be proposed only for non-filing of returns.

- All pending GST returns must be furnished.

- Entire tax dues must be paid.

- Interest must be paid.

- Late fee must be paid.

- Compliance must be completed before the cancellation order is passed.

Practical Example

Suppose XYZ Traders has not filed GSTR-3B returns for several months.

The Proper Officer issues FORM GST REG-17 proposing cancellation.

Instead of submitting a lengthy explanation, XYZ Traders:

- files all pending GSTR-3B returns,

- files pending GSTR-1 returns wherever applicable,

- pays tax liability,

- pays interest,

- pays late fee.

Since the default has been completely rectified, the Proper Officer should drop the proceedings by issuing FORM GST REG-20 under the proviso to Rule 22(4).

Important Limitation of Rule 22(4)

This relief is available only until the cancellation order is passed.

Once FORM GST REG-19 has been issued cancelling the registration, Rule 22(4) no longer applies.

At that stage, the taxpayer must seek restoration through the provisions relating to revocation.

Revocation of Cancellation Under Section 30

If the registration has already been cancelled by the Proper Officer, the taxpayer may apply for revocation of cancellation under Section 30.

Revocation means restoring the cancelled GST registration.

However, revocation is available only where the cancellation was initiated by the Proper Officer. It is not available where the taxpayer has voluntarily cancelled the registration.

Conditions for Revocation

Before applying for revocation, the taxpayer must:

- file all pending returns,

- pay tax liability,

- pay interest,

- pay late fee,

- comply with any additional conditions prescribed under Rule 23.

Only after these compliances can the application be filed.

Time Limit for Filing Revocation Application

The application for revocation must be filed within the prescribed time under Section 30 and Rule 23.

The Government has, from time to time, issued various notifications extending or condoning delays for specified periods. Therefore, taxpayers should always verify the latest notifications before assuming that the limitation period has expired.

What Happens if the Time Limit Expires?

Many taxpayers become compliant after the limitation period for revocation has already expired.

Can they still get their registration restored?

The answer is yes, in appropriate cases, through the constitutional jurisdiction of the High Courts.

The latest Gauhati High Court judgment is a good example.

Gauhati High Court Judgment

Smt. Bina Taipodia v. Union of India & Others

Court: Gauhati High Court

Case No.: WP(C) No. 212 of 2026

Facts of the Case

The petitioner was carrying on business under a valid GST registration.

The department issued a Show Cause Notice on 07 October 2024 proposing cancellation because GSTR-3B returns had not been filed.

Subsequently:

- GST registration was cancelled on 29 May 2025.

- The petitioner claimed that the show cause notice had never been received.

- Thereafter, she filed all pending GST returns.

- She deposited the outstanding tax and penalty on 23 April 2026.

Despite complete compliance, restoration was denied because the application for revocation was filed beyond the prescribed limitation period.

Issue Before the Court

Whether GST registration cancelled due to non-filing of returns can be restored after the taxpayer has subsequently complied with all statutory requirements.

Observations of the Court

The Gauhati High Court made several important observations.

1. Complete Compliance Had Already Been Made

The petitioner had already:

- filed all pending returns,

- deposited tax,

- paid the required penalty.

Therefore, the original default had substantially been cured.

2. Rule 22 Reflects the Legislative Intent

The Court referred to the proviso to Rule 22(4), which allows cancellation proceedings to be dropped when pending returns are filed and tax dues are paid before cancellation.

Although the cancellation had already taken place in this case, the Court observed that the Rule demonstrates the legislative intent of encouraging compliance rather than permanently denying registration.

3. Cancellation Has Serious Civil Consequences

The Court observed that cancellation of GST registration has serious consequences for business.

Without registration, a taxpayer cannot effectively continue commercial activities or issue tax invoices.

Therefore, restoration should ordinarily be considered once statutory compliance has been achieved.

4. Earlier Judgments Were Followed

The Court relied upon its earlier judgment in Dug Rade v. Union of India, which itself followed earlier coordinate bench decisions involving cancellation under Section 29(2)(c).

The consistent judicial approach has been to protect genuine businesses where the taxpayer has subsequently become compliant.

Final Directions of the Court

The Gauhati High Court directed:

- the petitioner to submit an application for restoration within 20 days,

- the GST authorities to verify compliance,

- the authorities to restore registration in accordance with law if the compliance was found satisfactory,

- the entire exercise to be completed within four weeks.

Practical Takeaways

If You Receive a Show Cause Notice

Do not ignore it.

Immediately:

- File all pending returns.

- Pay tax dues.

- Pay interest.

- Pay late fee.

You may be able to save your registration under Rule 22(4) itself.

If Registration Has Already Been Cancelled

Immediately:

- File pending returns.

- Pay all statutory dues.

- Apply for revocation within the prescribed period.

Delay can significantly complicate the restoration process.

If Revocation Time Has Expired

All hope is not lost.

Where the taxpayer has become fully compliant, High Courts have granted relief in deserving cases, including the Gauhati High Court in Smt. Bina Taipodia v. Union of India. However, such relief is discretionary and depends on the facts of each case. Taxpayers should not assume that courts will condone every delay.

The GST law has evolved from being purely procedural to becoming increasingly compliance-oriented. The proviso to Rule 22(4) is a significant example of this approach, allowing taxpayers to avoid cancellation by simply filing pending returns and clearing all outstanding dues before the cancellation order is passed.

Even after cancellation, the law provides a statutory remedy through Section 30 for revocation. Where this remedy is no longer available due to limitation, judicial intervention may still be possible in deserving cases, as demonstrated by the Gauhati High Court in Smt. Bina Taipodia v. Union of India.

The most effective strategy, however, is proactive compliance. Taxpayers should respond promptly to cancellation notices, file pending returns without delay, and clear all statutory dues to avoid unnecessary litigation and ensure continuity of business.