Updated for FY 2026-27 | Includes Mandatory ISD Provisions

Businesses operating through multiple branches often face confusion regarding GST implications on stock transfers, employee cost allocation, management services, and Input Service Distributor (ISD) compliance.

Common questions include:

- Is GST applicable on branch transfers?

- Is GST payable when goods are transferred without consideration?

- What happens when Head Office supports branches in other States?

- When should businesses use ISD and when should they use Cross Charge?

In this detailed guide, we will explain the GST treatment of branch-to-branch and Head Office-to-Branch transactions with practical examples and recent developments relating to ISD.

What Does GST Say About Multiple Registrations?

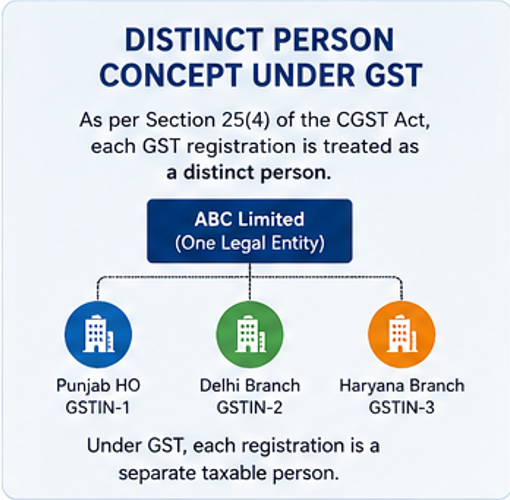

Distinct Person Concept Under GST

As per Section 25(4) of the CGST Act, 2017, where a person has obtained:

- More than one GST registration in one State or Union Territory, or

- GST registrations in different States,

each registration is treated as a distinct person.

Example

ABC Limited has:

| Location | GST Registration |

|---|---|

| Punjab Head Office | GSTIN-1 |

| Delhi Branch | GSTIN-2 |

| Haryana Branch | GSTIN-3 |

Although there is only one legal entity, GST treats each registration as a separate taxable person.

This concept is the foundation for understanding branch transfer taxation under GST.

Schedule I: GST Even Without Consideration

Generally, GST applies only when consideration exists.

However, Schedule I of the CGST Act specifies that:

Supply of goods or services between related persons or distinct persons in the course or furtherance of business shall be treated as supply even if made without consideration.

Therefore, GST may become applicable even when no money changes hands.

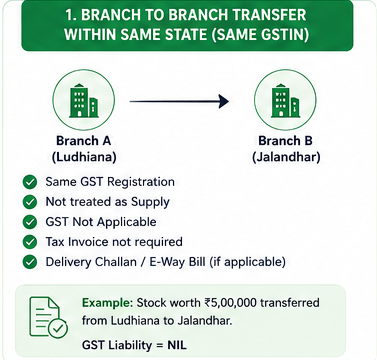

Scenario 1: Branch-to-Branch Transfer Within the Same State

Case Study

ABC Limited has:

- Branch A in Ludhiana

- Branch B in Jalandhar

Both branches operate under the same GST registration.

Goods are transferred from Ludhiana branch to Jalandhar branch.

GST Treatment

Since both locations are covered under the same GSTIN:

- Not treated as supply

- GST not applicable

- Tax invoice not required

Practical Position

Movement of goods within the same GST registration is merely an internal stock movement.

Documentation

Depending on the circumstances:

- Delivery Challan may be issued

- E-Way Bill may be required where applicable

Example

Stock worth ₹5,00,000 is transferred from Ludhiana branch to Jalandhar branch.

| Particulars | Amount |

|---|---|

| Value of Goods | ₹5,00,000 |

| GST Liability | NIL |

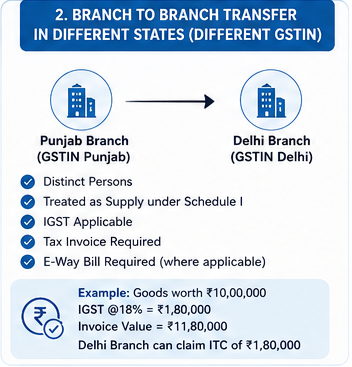

Scenario 2: Branch-to-Branch Transfer Between Different States

Case Study

ABC Limited transfers goods from:

- Punjab Branch (GSTIN Punjab)

to - Delhi Branch (GSTIN Delhi)

GST Treatment

Since both GST registrations are distinct persons:

- Transaction qualifies as supply

- Covered under Schedule I

- GST applicable even without consideration

Tax Applicable

Since the movement is interstate:

IGST will be charged.

Documentation Required

- Tax Invoice

- E-Way Bill (where applicable)

- Stock Transfer Records

Example

| Particulars | Amount |

|---|---|

| Goods Value | ₹10,00,000 |

| IGST @18% | ₹1,80,000 |

| Invoice Value | ₹11,80,000 |

Delhi Branch can claim ITC of ₹1,80,000 subject to normal conditions.

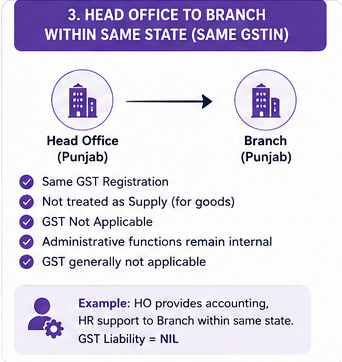

Scenario 3: Head Office to Branch Transfer Within the Same State

Case Study

Head Office and Branch are situated in Punjab and operate under a single GST registration.

Goods Transfer

Movement of goods between locations under the same GSTIN is not supply.

GST Liability = NIL

Administrative Functions

Head Office performs:

- Accounting

- Human Resources

- Legal Support

- Finance Functions

- Compliance Activities

for the branch.

Since both locations operate under the same GST registration, these remain internal functions and generally do not attract GST.

Example

Punjab Head Office maintains books of accounts for Punjab Branch.

GST Liability = NIL

Scenario 4: Head Office to Branch Transfer in Different States

Case Study

- Head Office located in Punjab

- Branch located in Delhi

Separate GST registrations have been obtained.

GST Treatment

Both registrations are distinct persons under Section 25.

Services provided by Head Office to Branch are treated as supply under Schedule I.

GST may be payable even if no amount is recovered from the branch.

Understanding Cross Charge Under GST

What is Cross Charge?

Cross Charge refers to the taxation of services supplied by one GST registration to another GST registration of the same legal entity.

Common Examples

Head Office provides:

- Accounting Services

- HR Services

- IT Support

- Treasury Functions

- Management Services

- Legal Assistance

to branches located in other States.

These services may require cross charging.

GST Implication

Punjab GSTIN raises tax invoice on Delhi GSTIN.

| Particulars | GST Impact |

|---|---|

| Service Supply | Taxable |

| Invoice Required | Yes |

| GST Applicable | IGST |

| ITC Available to Branch | Yes |

Understanding Input Service Distributor (ISD)

What is ISD?

Input Service Distributor (ISD) is a mechanism through which common input service credits are distributed among different GST registrations.

ISD does not involve supply of services.

It only distributes Input Tax Credit (ITC).

Typical Expenses Distributed Through ISD

Head Office receives invoices for:

- Statutory Audit Fees

- Software Licenses

- ERP Expenses

- Legal Consultancy

- Advertisement Expenses

- Insurance Policies

- Cloud Subscription Charges

These services are commonly used by multiple branches.

ISD vs Cross Charge – Key Differences

| Particulars | ISD | Cross Charge |

|---|---|---|

| Purpose | Distribution of ITC | Taxation of Supply |

| Applicable For | Common Input Services | Services supplied by HO |

| Invoice Type | ISD Invoice | Tax Invoice |

| Output Tax Payment | Not Required | Required |

| ITC Distribution | Yes | No |

| Supply Involved | No | Yes |

Major Change: Mandatory ISD from 1 April 2025

The Finance Act has strengthened ISD provisions and businesses receiving common input service invoices at Head Office are now required to distribute eligible ITC through ISD mechanism.

Common Examples

Where invoices are received for:

- Audit Fees

- Corporate Consultancy

- Group Insurance

- ERP Software

- Advertisement Campaigns

- Cloud Infrastructure

the related ITC should generally be distributed through ISD.

When Should Businesses Use ISD?

Use ISD where:

- Invoice is received from an external vendor.

- Credit pertains to multiple GST registrations.

- Head Office merely receives the invoice and distributes credit.

Example

Audit Fee = ₹3,00,000

Beneficiaries:

- Punjab Branch

- Delhi Branch

- Haryana Branch

Input Tax Credit should be distributed through ISD.

Valuation of Branch Transfers

Applicable Provision

Valuation is governed by:

- Section 15 of CGST Act

- Rule 28 of CGST Rules

Open Market Value Method

Generally, valuation should be based on Open Market Value (OMV).

Full ITC Relief

Rule 28 contains a major relaxation.

Where the recipient branch is eligible for full ITC:

The value declared in the invoice shall be deemed to be the open market value.

This provision significantly reduces valuation disputes in branch transfers.

Documents Required for Branch Transfers

Interstate Stock Transfer

- Tax Invoice

- E-Way Bill

- Stock Transfer Records

- Accounting Entries

ISD Compliance

- ISD Registration

- ISD Invoice

- Credit Distribution Working

- Vendor Tax Invoices

Practical Compliance Checklist

Before closing monthly GST books, businesses should verify:

✅ Interstate stock transfers invoiced properly

✅ E-Way Bills generated where required

✅ Cross-charge transactions identified

✅ Common service credits distributed through ISD

✅ Valuation documentation maintained

✅ Branch-wise ITC reconciliation completed

The GST implications of branch-to-branch and Head Office-to-Branch transactions depend primarily on whether the locations operate under the same GST registration or under separate GST registrations.

While transfers within the same GSTIN generally remain outside GST, transactions between distinct persons are taxable under Schedule I even when no consideration is charged.

Businesses having multiple registrations should establish a clear framework for:

- Stock Transfers

- Cross Charge Compliance

- ISD Credit Distribution

- Documentation

- Valuation

With the mandatory ISD regime now in force, organizations must carefully distinguish between distribution of common ITC through ISD and taxable services requiring Cross Charge to ensure complete GST compliance and avoid future litigation.