Under GST, goods are generally required to be accompanied by a Tax Invoice when they are supplied. However, there are several situations where issuing a tax invoice at the time of movement of goods is either impractical or not legally required.

To address such situations, Rule 55 of the CGST Rules, 2017 permits the movement of goods under a Delivery Challan instead of a tax invoice.

Businesses frequently use delivery challans for:

- Job work transactions

- Transportation of liquid gas

- Movement of goods for reasons other than supply

- Transfer of goods where quantity is not known at the time of dispatch

- Semi-finished goods sent to another unit for processing

Understanding Rule 55 is important because incorrect documentation during movement of goods can result in detention of goods and vehicles under GST.

What is a Delivery Challan?

A Delivery Challan is a document issued for the movement of goods when a tax invoice is not required to be issued at the time of dispatch.

It serves as documentary evidence explaining the purpose of transportation and contains prescribed particulars under GST law.

Legal Provision

Rule 55(1) of the CGST Rules, 2017 provides that goods may be transported on a Delivery Challan instead of a Tax Invoice in specified situations.

When Can Goods Be Transported on a Delivery Challan?

A Delivery Challan may be issued in place of a Tax Invoice in the following cases:

1. Supply of Liquid Gas Where Quantity is Not Known at the Time of Removal

In certain industries, the exact quantity of gas supplied can only be determined after delivery.

Example

A gas manufacturing company dispatches liquid oxygen in a tanker.

At the time of removal from the factory, the exact quantity deliverable to the customer is not ascertainable.

The company can transport goods using a Delivery Challan and issue the Tax Invoice after actual quantity determination.

2. Transportation of Goods for Job Work

Goods sent to a job worker can be moved under a Delivery Challan.

Example

A manufacturer sends steel sheets to a job worker for cutting and fabrication.

Since ownership remains with the principal and no supply takes place, the movement can be covered by a Delivery Challan.

3. Transportation of Goods for Reasons Other Than Supply

This is one of the most commonly used clauses.

Examples include:

- Goods sent for exhibition

- Goods sent for testing

- Goods sent for repair

- Goods sent on approval basis

- Branch-to-branch movement without supply

- Tools and equipment transported to a work site

- Machinery sent for demonstration

Example

A company sends machinery to a trade exhibition in another state.

Since no sale occurs at the time of dispatch, the goods may move under a Delivery Challan.

4. Other Supplies as Notified by the Board

CBIC may notify additional situations where delivery challan can be used instead of a tax invoice.

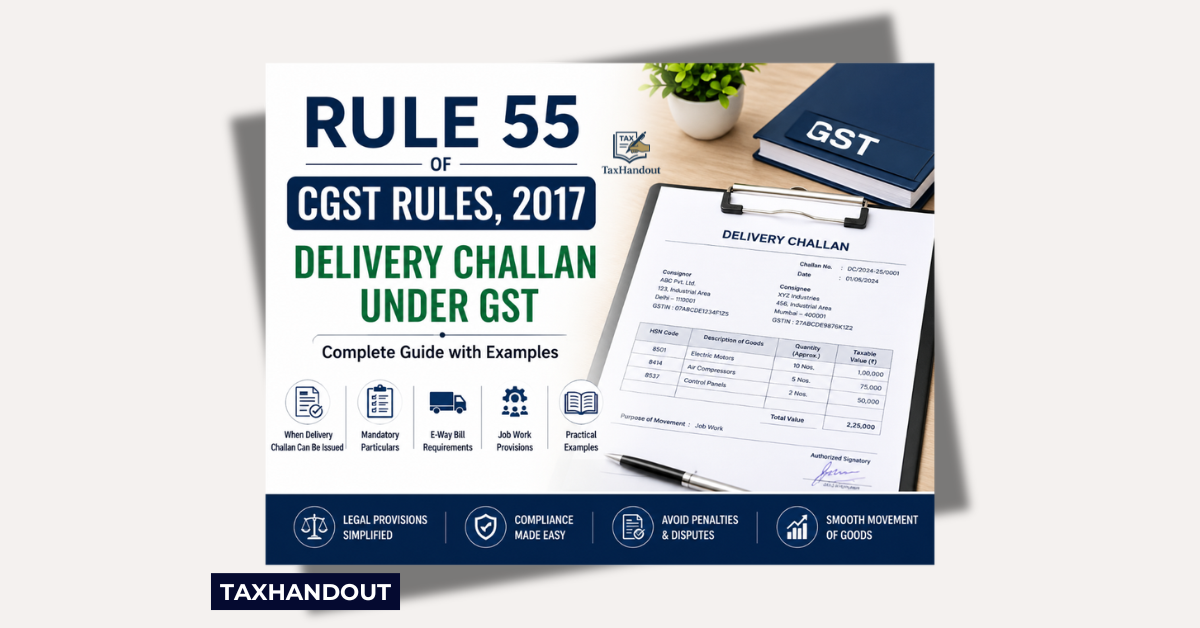

Mandatory Particulars of Delivery Challan

As per Rule 55(1), a Delivery Challan must contain the following details:

| Particulars | Required |

| Date and Number of Delivery Challan | Yes |

| Name, Address and GSTIN of Consignor | Yes |

| Name, Address and GSTIN/UIN of Consignee (if registered) | Yes |

| HSN Code and Description of Goods | Yes |

| Quantity (Provisional if exact quantity not known) | Yes |

| Taxable Value | Yes |

| Tax Rate and Tax Amount (where transportation is for supply) | If applicable |

| Place of Supply (Inter-State movement) | If applicable |

| Signature of Authorized Person | Yes |

The Delivery Challan should be serially numbered and unique for a financial year.

Number of Copies of Delivery Challan

Rule 55(2) requires preparation of the Delivery Challan in triplicate:

| Copy | Purpose |

| Original | Consignee |

| Duplicate | Transporter |

| Triplicate | Consignor |

Delivery Challan and E-Way Bill

A common misconception is that an e-way bill is not required when goods move under a Delivery Challan.

This is incorrect.

If the value of goods exceeds the prescribed e-way bill threshold, the e-way bill provisions apply even when goods are transported under a Delivery Challan.

Example

A manufacturer sends machinery worth ₹5 lakh to a job worker.

Documents required:

- Delivery Challan

- E-Way Bill (if applicable)

Both documents should accompany the goods.

Rule 55(3): Transportation in Semi-Knocked Down (SKD) or Completely Knocked Down (CKD) Condition

Certain machinery or large equipment cannot be transported in a single vehicle.

Rule 55(3) provides a special procedure.

Requirements

First Consignment

- Complete Tax Invoice must be issued before dispatch.

- Original Invoice accompanies the first consignment.

Subsequent Consignments

- Delivery Challan referring to the original invoice.

- Certified copy of invoice accompanies each subsequent consignment.

Last Consignment

- Original invoice should accompany the final consignment.

Example

A large industrial plant worth ₹2 crore is transported through five trucks.

One tax invoice may be issued for the entire supply, while individual consignments move under delivery challans referencing the original invoice.

Delivery Challan for Job Work – Practical Understanding

One of the most frequent uses of Rule 55 is in job work transactions.

Movement covered:

Principal → Job Worker

Delivery Challan

Job Worker → Another Job Worker

Delivery Challan

Job Worker → Principal

Delivery Challan

Job Worker → Customer (where permitted)

Delivery Challan along with applicable GST documentation.

Difference Between Tax Invoice and Delivery Challan

| Particulars | Tax Invoice | Delivery Challan |

| Used for Supply | Yes | Generally No |

| GST Liability Arises | Yes | Usually No |

| ITC Claim Basis | Yes | No |

| Records Sale Transaction | Yes | No |

| Used for Job Work | No | Yes |

| Used for Exhibition/Testing | No | Yes |

Rule 55 of the CGST Rules provides a practical mechanism for transporting goods in situations where issuing a tax invoice at the time of movement is either impossible or unnecessary. Delivery Challans play a crucial role in job work transactions, exhibition movements, testing activities, repairs, and transportation of liquid gas.

However, taxpayers should remember that a Delivery Challan is not a substitute for a Tax Invoice in genuine supply transactions. Proper documentation, compliance with e-way bill provisions, and inclusion of all mandatory particulars are essential to avoid penalties and disputes during transit inspections.

A clear understanding of Rule 55 helps businesses ensure smooth movement of goods while remaining fully compliant with GST law.